Double materiality assessment (DMA) has become a key tool for structuring sustainability information and understanding which impacts, risks and opportunities should be prioritised by an organisation. In this process, matrices, internal workshops, stakeholder interviews and prioritisation methodologies play an important role: they help structure the assessment, compare perspectives and organise conclusions. Their value increases when they are integrated into a broader, traceable and evidence-based process capable of explaining why certain issues are relevant, why others are not, and how these conclusions can inform management decisions.

From this perspective, double materiality should be understood as a roadmap for identifying, assessing and substantiating the impacts, risks and opportunities that are most relevant to the company, beyond a visual output or a standalone prioritisation exercise.

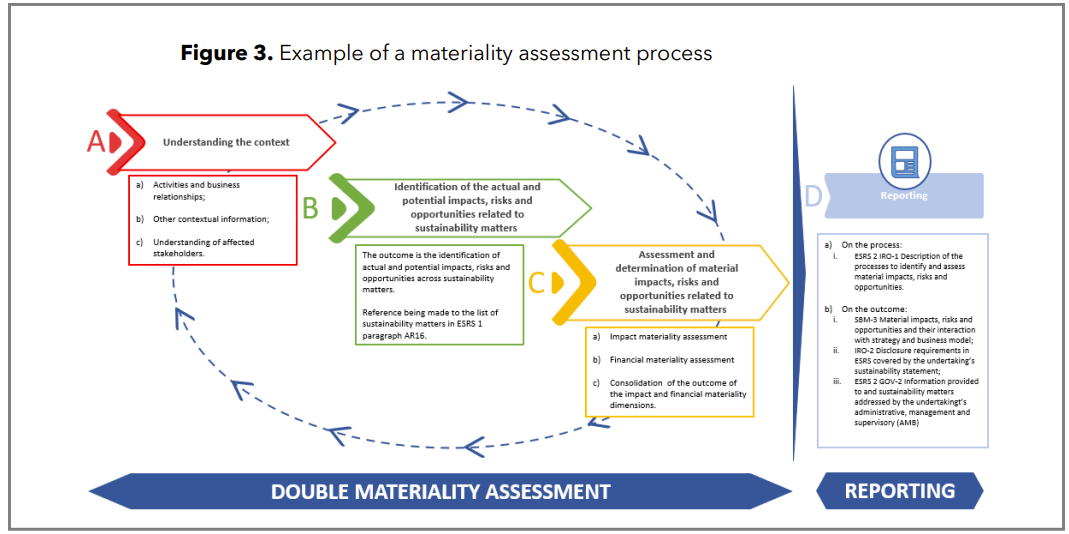

This idea aligns well with the methodological logic proposed by EFRAG in IG 1 (Materiality Assessment Implementation Guidance) on materiality assessment, which remains a practical reference for structuring the process: understanding the context, identifying impacts, risks and opportunities, assessing their materiality, and documenting the reasoning followed.

The simplification proposals published by EFRAG in July 2025 introduce nuances that deserve careful attention. Without replacing the existing methodology or anticipating definitive conclusions, these proposals reinforce principles such as proportionality, reasonable evidence and the need to focus the assessment on what is genuinely relevant to the organisation. In practice, this approach invites a distinction between documentary accumulation and rigour: what matters is not demonstrating that everything has been analysed with the same level of depth, but being able to reasonably justify why certain issues are, or are not, material.

With this idea in mind, it is worth revisiting the usual steps of double materiality assessment and pausing on certain aspects that, while fundamental, often remain in the background.

Principles that help interpret double materiality assessment

Principle of proportionality

The principle of proportionality involves adapting the depth and scope of the assessment to the organisation’s characteristics: its size, sector, operational complexity, value chain, exposure to specific impacts or risks, and availability of information. In practice, this means adjusting the level of detail and intensity of the assessment to the needs of each organisation and the issues being addressed.

However, proportionality should not be confused with indiscriminate simplification. Nor does it mean reducing the rigour of the exercise or analysing less by default. Rather, it means dedicating greater depth where there are stronger indications of relevance and avoiding disproportionate efforts on issues whose exposure or potential impact appear limited.

From this perspective, a proportionate assessment is one that concentrates time, resources and technical capacity where they genuinely add value.

Reasonable evidence

In practical terms, this means that the conclusions of the assessment should be based on sufficient, consistent and defensible information, even when that information is not perfect or fully exhaustive.

This evidence may come from multiple sources: the organisation’s internal information, sector-specific regulation, benchmarks, scientific studies, expert knowledge, territorial analyses, value chain information or previous exercises carried out by the company.

Rather than gathering all possible information, the objective is to have a solid basis for justifying which issues are considered material and which are left outside the assessment.

This introduces an important nuance. In addition to identifying priorities, double materiality also requires the ability to explain the reasoning followed. Why is a topic considered material? What information supports that conclusion? What uncertainties exist? What evidence supports the conclusion that another issue is not a priority?

In other words, the quality of the assessment depends as much on its results as on the ability to reasonably justify how those results were reached.

A practical roadmap for double materiality assessment

1. Understanding the organisation’s context

A common interpretation is to think that the assessment begins when a workshop is organised, an internal survey is launched or different departments come together to assess sustainability-related issues. However, double materiality starts earlier: with an understanding of the context in which the organisation operates.

Before assessing impacts, risks or opportunities, it is necessary to understand how the business model works, what products and services are offered, which resources are used, how the value chain is structured, where the organisation operates and which regulatory, environmental or market dependencies may influence its activities. It is also useful to consider which regulatory, technological or sectoral changes could alter that context in the short, medium or long term.

This stage involves turning the knowledge that the organisation already has about itself into an explicit and defensible basis, documenting the information used, its origin, scope and contribution to the identification of impacts, risks and opportunities. This foundation makes it possible to understand why certain issues are included in the assessment while others remain in the background. Although this step may seem less visible than later prioritisation, it is one of the most decisive for the quality of the final outcome.

2. Identifying potential impacts, risks and opportunities

Once the context has been understood, the next step is to identify the impacts, risks and opportunities that may be relevant to the organisation. This stage acts as a bridge between business understanding and the subsequent materiality assessment: the objective is not yet to decide what is material, but rather to define which issues are worth analysing in greater depth.

At this stage, it is important to avoid two relatively common extremes. The first is transferring generic sustainability lists into the assessment without grounding them in the organisation’s specific reality. The second is attempting to cover every possible issue with the same level of detail, resulting in exercises that are overly complex, disproportionate and difficult to sustain over time.

The identification of impacts, risks and opportunities requires combining business knowledge, sector context and an understanding of the dynamics that may influence the organisation, from regulatory changes to resource dependencies, market transformations or growing expectations across the value chain. The objective is to build a reasonable and defensible basis of potentially relevant issues, tailored to the organisation’s context and capable of serving as a starting point for the subsequent materiality assessment.

At this point, the principle of proportionality becomes relevant again, understood as a way to maintain rigour in the assessment while focusing attention on the issues with the strongest indications of relevance.

3. Assessing materiality using defensible criteria

Once potential impacts, risks and opportunities have been identified, one of the most important stages of the process begins: assessing which of them reach a sufficient level of materiality to inform the organisation’s reporting and management.

At this stage, the key issue is being able to explain why certain matters are considered material from an impact perspective, a financial perspective or both. This means that conclusions should be supported by a comprehensible logic: which elements have been taken into account, what level of uncertainty exists and why the assessment reached is reasonable for that organisation and its context.

From this perspective, assessing materiality means building a defensible conclusion, avoiding a mechanical application of scoring systems. The same issue may present very different levels of relevance depending on the activity, value chain, regulatory exposure, location or market evolution. Therefore, prioritisation should be based on an assessment capable of connecting the company’s context with the identified impacts, risks and opportunities.

Ultimately, a robust assessment combines a clear prioritisation of issues with a reasoned explanation of the criteria that justify the level of relevance assigned to each one.

4. Justifying what is not material as well

One aspect that often receives less attention in double materiality assessments is the justification of those matters that are ultimately not considered material. The assessment should identify priorities while also providing a reasoned justification for which impacts, risks or opportunities fall below the materiality threshold for an organisation.

In some cases, non-materiality is interpreted simply as whatever does not appear in the final matrix. From a technical perspective, this reading is insufficient. A matter not being material should not mean that it has not been considered, but rather that, after analysing it in relation to the company’s context, insufficient elements have been identified to consider it a priority.

This is where reasonable evidence becomes important again. The assessment should include a coherent explanation capable of supporting the conclusion reached. This is especially relevant for matters that may appear important in general terms, but whose material relevance depends heavily on the sector, activity, locations, value chain or specific exposure of the organisation.

Non-materiality should therefore be understood as a reasoned conclusion. And precisely for this reason, in many cases, the ability to explain why something is not material can be as relevant as justifying why another matter is.

5. Documenting the reasoning and ensuring traceability

A robust double materiality assessment should make it possible to reconstruct the reasoning followed throughout the process.

This involves documenting, in a proportionate manner, which information has been considered, which sources have supported the assessment, which assumptions have been made, which uncertainties have existed and which criteria have ultimately led to some matters being considered material and others not. The objective is to preserve the logic underpinning the decisions taken.

Traceability serves a practical purpose. It adds consistency to the assessment, facilitates future updates and makes it possible to explain the reasoning followed when the context changes, priorities are reviewed or internal and external questions arise regarding the conclusions reached.

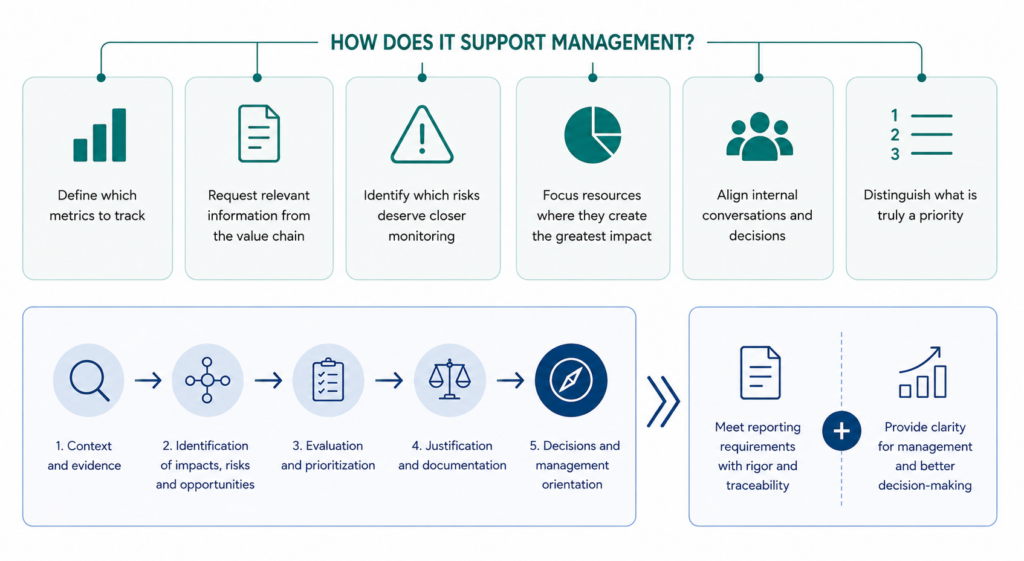

Connecting DMA with management

A simple way to assess whether a double materiality assessment is adding value is to ask whether its results help support better decision-making within the organisation. This does not mean that every conclusion must immediately translate into a new policy, metric or action, but rather that the assessment helps structure priorities and guide management more clearly.

When the exercise is well connected to management, it can help define which metrics are worth tracking, what information it is relevant to request from the value chain, which risks deserve closer monitoring or where it makes sense to focus resources. It can also contribute to aligning internal conversations, avoiding the treatment of all sustainability matters with the same level of priority.

Double materiality should be understood as a chain of reasoning that makes it possible to explain, justify and use the decisions taken. Its value lies in a dual function: responding to reporting requirements while also providing clarity for management.

Insights sugeridos

Scope 3 carbon footprint: towards a more representative assessment of supply chain emissions

How to Start Assessing Physical and Transition Climate Risks in the Shift to a Low-Carbon Economy

Evaluating impacts on nature: state metrics and biodiversity footprint